Biodiversity credits for nature capital: What CSOs need to know

Biodiversity credits are emerging as a new mechanism to increase capital for nature protection and could soon be an additional instrument in the Chief Sustainability Officer’s toolbox – as long as they understand their risks and benefits.

Judging by the recent wave of nature and biodiversity commitments among global firms, as well as the new roles being created to lead these efforts, companies are starting to adopt a more holistic approach to climate action. Biodiversity disclosures have doubled among US-listed companies, and 320 firms worth US$4 trillion are due to publish their first nature-related disclosures aligned with the TNFD framework by the end of 2026.

This shift is largely the result of the Kunming-Montreal Global Biodiversity Framework signed in 2022, which aims to restore 30% of degraded land and marine ecosystems globally by 2030. Governments had so far provided as much as 83% of global nature finance, but this agreement made it clear that achieving biodiversity goals would require much more private sector participation, starting with monitoring and disclosing nature impacts.

But the deal also had financial objectives: to redirect US$500 billion of harmful government subsidies toward biodiversity and mobilise an additional US$200 billion per year “from all sources” for conservation and restoration. (In 2022, just US$35 billion was invested in nature-based solutions, compared to US$5 trillion that went into projects that harmed nature and biodiversity.)

As such, the Global Biodiversity Framework states that countries should promote blended finance and encourage the private sector to invest in biodiversity, including through innovative mechanisms such as biodiversity credits.

How biodiversity credits work

Like carbon credits, biodiversity credits aim to measure the positive impacts of a project and package them into sellable units to increase investment in such project – but while carbon credits focus purely on emissions, biodiversity credits must monitor a wide range of metrics that vary depending on location and type of ecosystem.

As such, there currently isn’t one standard methodology to create biodiversity credits. Instead, different organisations are coming up with different criteria and metrics to develop these units.

For example, one Colombian company, Terrasos, is selling voluntary biodiversity credits emitted in the Bosque de Niebla - El Globo Habitat Bank to private firms: each €35 credit represents 30 years of conservation and restoration on 10 square metres of forest.

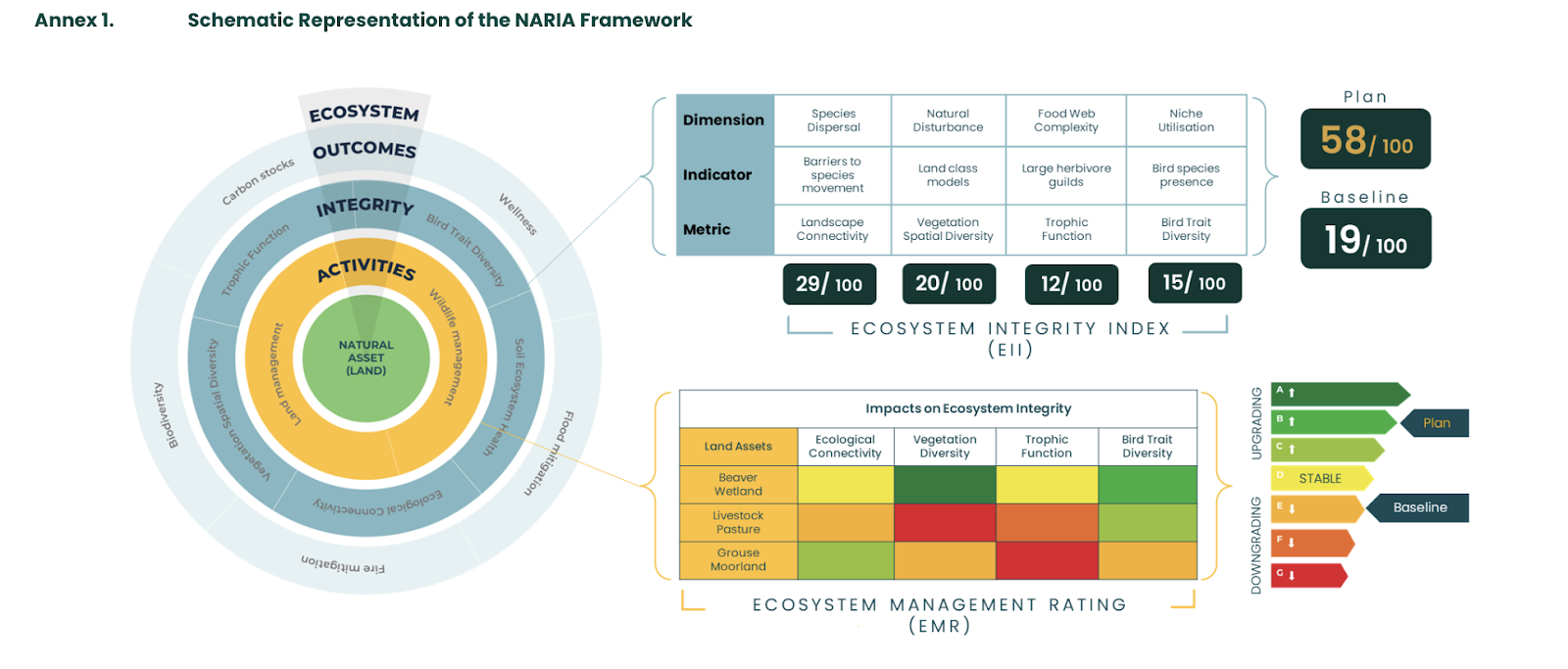

Elsewhere, Innovate UK-backed CreditNature has developed a framework to measure the ecosystem benefits of nature investment called Natural Assets Recovery Investment Analytics, of NARIA.

The framework (which is currently focused on land ecosystems) uses four metrics to measure impact: landscape connectivity – ie, the removal of barriers such as fences and roads to allow for the free movement of species and nutrients; vegetation spatial diversity; trophic function – the presence of large herbivores and the effect their presence has on the entire food web; and bird trait diversity, which is an indicator of the resources that available to those birds.

Each nature credit generated through CreditNature’s projects represents a one point uplift in natural assets recovery over one hectare, explains Ed Pragnell, Nature Finance Lead.

In April, NARIA’s Terrestrial Ecosystem Condition Method became the first ecosystem restoration measurement framework to be accredited by the Accounting for Nature Standard. “That's a huge feather in our cap and hopefully provides that trust and confidence to the buyers of these credits,” Pragnell tells CSO Futures.

Demand for biodiversity credits remains slow

CreditNature is six months into a pre-commercial agreement with the Scottish Government to create the market infrastructure for a nature credit market. “What we're designing is an end-to-end system through which private capital or institutional capital, so corporates and financial institutions, can invest into nature restoration projects, in return for nature credits,” he explains.

August 2024 will mark the end of the pre-commercial agreement, which CreditNature hopes to turn into a commercial agreement “whereby we will have a code or standard which is endorsed by the Scottish Government on large-scale ecosystem restoration, and through which the credits for that system will be recognised by them as being valid under emerging sustainability disclosure requirements”.

Pragnell believes this type of government backing would help de-risk the biodiversity credit market and create trust with companies that may be wary of repeating the mistakes of the voluntary carbon market.

“We've got interest, but there's no one actually reaching their hand into their pocket yet and putting money on the table, for a number of reasons. I think one of them is ‘why should we do this without any mandatory regulatory requirements?’ Another one is just the risk appetite: it's a very new market. We have an accredited index, but we're not endorsed by any sort of public body yet, so it's kind of that sort of trust issue still, and certainly on the back of some of the pull downs we've seen in the carbon markets,” he says.

Demand also seems to be slow for Terrasos: its Bosque de Niebla project was launched two years ago with just 345 biodiversity credits put out for sale – yet these remain widely available on its commercial partner’s platform today, and the company is now looking to list the same credits on additional platforms. (It took Terrasos six years to sell 600 biodiversity credits from another of its habitat banks.)

Still, BloombergNEF estimates that biodiversity-related offsets and credits mobilise US$6-9 billion a year, with US$8 million committed to eight of the most developed biodiversity credit schemes (including Terrasos) as of May 2023.

Companies that do choose to invest in this new mechanism mostly target reputational and engagement benefits: “The bulk of the interests we’re getting from corporates are those who want to be ahead of the curve, who want the reputational benefit of having invested in these ecosystem recovery projects,” adds Pragnell. “And you can demonstrate the benefits of those projects to their stakeholders, which will help engage with employees, supply chain, shareholders and customers as well.”

Government oversight and standardisation of the biodiversity credit market

Market players are advocating for increased government oversight as a way to create trust in the market, making biodiversity credits a more powerful instrument to drive nature capital. But specialists warn that this scrutiny should be focused on guaranteeing the environmental benefits of biodiversity credits – not on mandating their use.

“Recently, it seems there is a push to lobby governments to scale biodiversity credit markets through regulation, which is very problematic,” notes Emil Sirén Gualinga, a natural resources researcher at the Business & Human Rights Resource Centre.

In a policy brief published this May, he calls on governments to halt biodiversity offsetting and the scaling of biodiversity credits through regulation, referring to a Third World Network paper questioning their effectiveness in protecting biodiversity and the communities who depend on it.

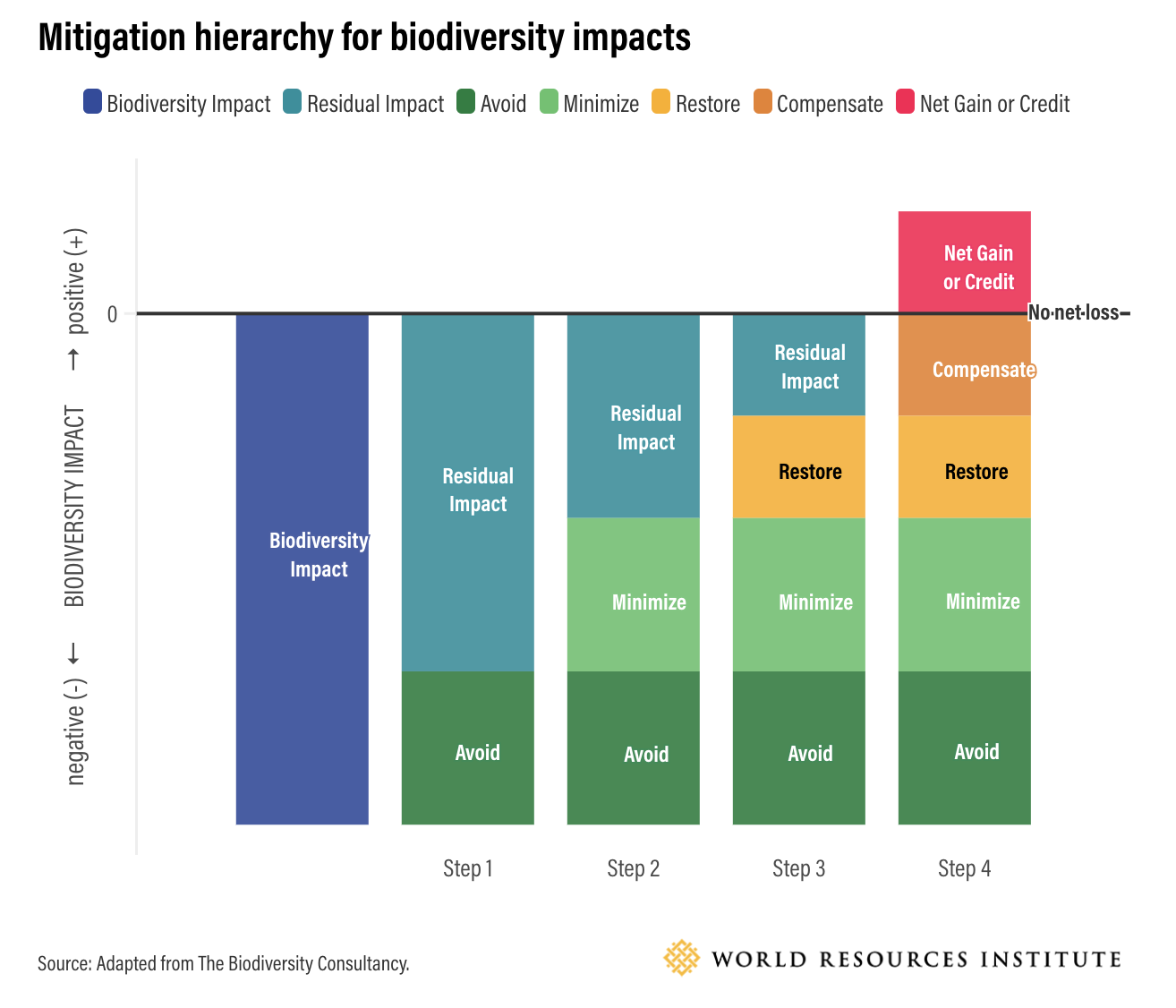

One of the points made by Third World Network researchers is that most of the biodiversity offset schemes in existence today “do not subscribe to the mitigation hierarchy”, meaning that they allow firms to compensate for their negative impacts on nature without first avoiding and mitigating them “because it is cheaper and faster for firms to pay for compensation rather than to avoid or mitigate biodiversity loss”.

Incentivising the biodiversity offsetting market could lead to artificial demand and land grabbing affecting Indigenous Peoples, yet their effectiveness to restore natural ecosystems has yet to be consistently proven, Sirén Gualinga adds.

For this reason, many participants argue that biodiversity credit usage should remain voluntary and based on the principles of “nature positivity”: not used to offset impacts, but rather to go the extra mile after measures are taken to limit them. “We don't want corporates who are doing damage elsewhere in the world to buy our credits to justify the damage that they're doing,” notes Pragnell.

The Taskforce for Nature-Related Financial Disclosure (TNFD), one of the main organisations driving standardised natural impact assessment among companies, seems reluctant to take an active role in the development of biodiversity credits. Pragnell says he has “had no luck” connecting with members of the team to discuss where the TNFD approach can align with CreditNature’s system, and the organisation also declined to be interviewed for this article – though it does recommend that companies disclose the “value of total biodiversity offsets purchased and sold” after applying the mitigation hierarchy.

Biodiversity credits for nature capital: 'not a magic wand’

Speaking at a recent S&P Global Sustainable1 webinar on unlocking capital for nature, David Vaillant, Global Head of Finance, Strategy and Participations at BNP Paribas Asset Management and a member of the International Advisory Panel on Biodiversity Credits (IAPB), explained that more awareness needs to be created around “the tool that these biodiversity credits can possibly represent”.

“This may be just one way of contributing to and channelling money towards biodiversity protection and restoration – and it may not be the largest. I don't think we should think about these credits, if they really come to fruition, as a magic wand,” he added.

The IAPB is working to map existing biodiversity credits around the globe to identify common features and come up with “sound principles” to adopt if they were to scale. This, according to Vaillant, involves understanding how, where and how often to measure biodiversity impact, as well as the drivers of demand from corporates, in order to drive trust – though he warns that “this is very experimental, in the sense that measuring nature is something that we should all acknowledge is difficult”.

For that reason, he seems against the creation of a “global market with homogeneous tradable units”, instead preferring a close link between projects and companies, who would use these credits only “after proper mitigation actions have been taken”.

Sirén Gualinga also believes international, cross-ecosystem or distant biodiversity offsetting mechanisms should be banned – and he is calling for standardising bodies such as IAPB and the Biodiversity Credit Alliance to “explicitly state in their recommendations that biodiversity credits should remain fully voluntary”.

It is clearly too early for companies to make biodiversity credits an integral part of their nature strategy, but the immaturity of this market presents an opportunity to influence its development. For example, the IAPB is running an open consultation until May 24 on possible market models for biodiversity credits and the “key features that could influence their success” – a chance for firms and their Chief Sustainability Officers to advocate for local, community-driven, verified and voluntary biodiversity credits as a driver for corporate nature action before the next ‘biodiversity COP’ in Colombia.

Member discussion